Bad money habits can quietly drain finances even for people who work hard and earn regularly. Many working adults experience the same frustrating cycle: payday arrives, bills get paid, small purchases add up, and suddenly the money feels gone again. While inflation and rising living costs play a major role, everyday financial habits can also slowly create long-term financial stress without people realizing it immediately.

For many working adults, payday no longer feels exciting the way it used to. The salary arrives, bills get paid, a few “small” purchases happen throughout the week, and suddenly the money feels thin again. Some people blame inflation immediately. Others blame low income. But in many cases, financial stress is also shaped by quiet habits that slowly drain stability over time.

Money problems are deeply emotional, even if people rarely talk about them that way. Spending is often connected to stress, insecurity, exhaustion, pressure, or the desire to feel rewarded after surviving another difficult workweek. That’s part of why financial struggle can feel frustratingly repetitive. A person may genuinely work hard and still feel stuck because certain behaviors have become automatic without them realizing how much damage they create in the long run.

One of the biggest habits that keeps people financially struggling is emotional spending. After stressful commutes, toxic workdays, or exhausting overtime shifts, many people look for quick comfort. Sometimes it comes through online shopping late at night. Sometimes it’s expensive food deliveries that feel deserved after a difficult day. A small purchase can temporarily create relief or excitement, which is why emotional spending becomes addictive so quietly. The problem is that the emotional reward usually lasts minutes, while the financial consequences stay much longer. Studies on emotional spending habits show that stress and emotions can strongly influence purchasing behavior

Lifestyle inflation is another common trap, especially among young professionals finally earning more money than before. A raise should ideally create financial breathing room, but many people immediately upgrade their lifestyle once their income increases. A perfectly functional phone suddenly feels outdated. Weekends become more expensive. Dining out becomes routine instead of occasional. New monthly subscriptions quietly pile up. Over time, expenses rise so naturally that a higher salary no longer feels like progress.

Small daily spending habits also damage finances more than many realize. A ₱180 coffee during work breaks, convenience store snacks during stressful afternoons, random online checkouts during flash sales, or ride-hailing services to avoid traffic may not seem serious individually. But repeated consistently, these habits quietly consume thousands of pesos every month. Many people only realize the impact when they ask themselves where their salary actually went and struggle to find a meaningful answer.

Another dangerous habit is depending too heavily on credit cards and digital lending apps. According to consumer finance studies in several Asian markets, short-term digital borrowing has grown rapidly because it offers instant relief during financially difficult periods. The problem is that convenience can easily hide long-term consequences. Minimum payments create the illusion that debt is manageable while interest quietly grows in the background. Understanding credit card interest and debt can help people avoid long-term financial pressure caused by unpaid balances. Some workers eventually reach a point where a large percentage of every paycheck already belongs to unpaid balances before the money even arrives.

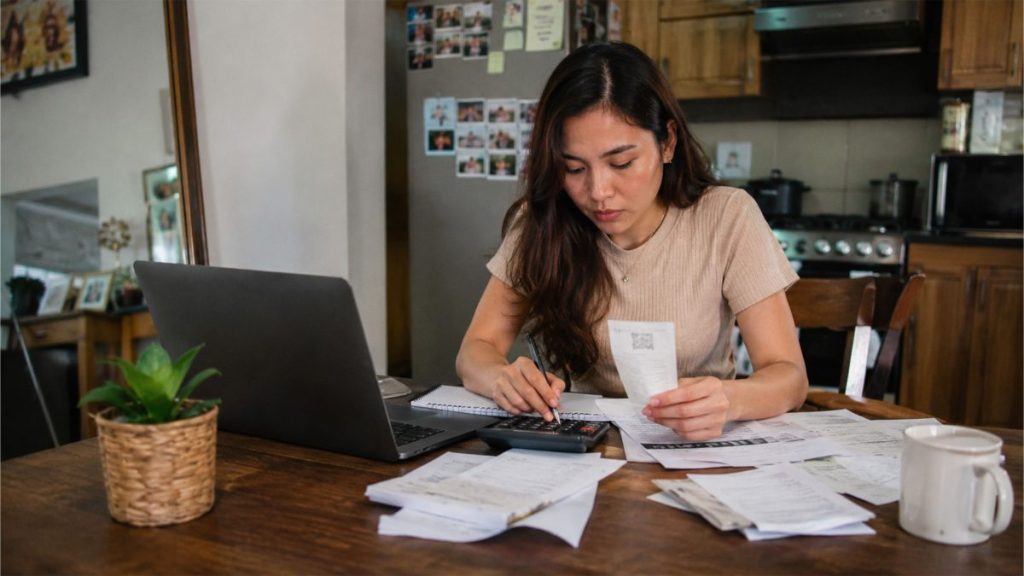

Avoiding budgeting is another reason many people remain financially unstable despite earning regularly. Some avoid tracking expenses because they believe budgeting feels restrictive or stressful. Others simply fear confronting how much they spend emotionally. But financial uncertainty often creates more anxiety than budgeting itself. People are frequently surprised when they finally write down their monthly expenses and discover how much money disappears into habits they barely notice anymore.

Social media has also changed the emotional relationship many people have with money. Constant exposure to vacations, luxury restaurants, gadgets, skincare hauls, and curated lifestyles creates silent pressure to appear financially successful. A person scrolling through social media after work may suddenly feel dissatisfied with their own life, even if they were financially stable an hour earlier. This emotional comparison quietly pushes some people into unnecessary spending simply to avoid feeling left behind.

Delaying savings until “later” is another habit that causes long-term financial problems. Many people convince themselves they will start saving after receiving a better salary, finishing debt payments, or reaching a more stable phase in life. But financial discipline rarely appears overnight. In reality, people who struggle to manage smaller incomes often continue struggling even after earning more because the underlying habits never changed.

Ignoring emergency savings can also become financially devastating. Medical emergencies, sudden unemployment, family crises, or unexpected repairs rarely arrive at convenient times. Without savings, even relatively small emergencies can quickly spiral into overwhelming debt. Building an emergency fund is often considered one of the most important steps toward financial stability. Financial stress becomes heavier when a person knows there is no safety net protecting them from one bad month turning into a major crisis.

Another habit keeping many people financially stuck is chasing unrealistic shortcuts to wealth. Social media is filled with people selling overnight success stories, questionable investment opportunities, and lifestyles designed to look effortlessly rich. Some individuals become trapped constantly searching for a financial breakthrough instead of building slow but stable habits. This mindset often leads to impulsive investments, burnout from multiple side hustles, or falling for schemes that promise easy money during vulnerable moments.

Avoiding honest conversations about money also creates problems that quietly grow over time. In many families, debt and financial hardship are treated like personal shame instead of normal struggles that can be improved with planning and discipline. Some people avoid checking their bank accounts because low balances trigger anxiety. Others hide debt from partners or relatives because they fear judgment. But avoiding financial reality rarely protects anyone from consequences. In most cases, silence simply delays solutions.

For many Filipinos, financial pressure also comes from family responsibility. Breadwinners often carry enormous emotional weight while trying to support parents, siblings, relatives, or younger family members. Helping loved ones is deeply rooted in Filipino culture and often comes from genuine love. But without boundaries, some people eventually become trapped in a cycle where they continuously rescue others while quietly neglecting their own financial stability. The pressure to always provide can become emotionally exhausting, especially when nobody notices the burden being carried.

What makes these habits dangerous is that most of them feel normal. Financial struggle rarely appears all at once. More often, it develops slowly through routines people stop questioning. Emotional spending becomes part of stress relief. Debt becomes routine. Saving money keeps getting postponed. Financial anxiety slowly becomes part of everyday life until people start believing constant stress is simply normal adulthood.

The good news is that financial habits can change, even gradually. Most people who improve their financial situation do not suddenly become wealthy overnight. Instead, they become more aware of the emotional patterns behind their spending. They learn how to pause before impulse purchases. They stop trying to impress people who are not paying their bills. They become more intentional with decisions that once happened automatically.

Real financial stability is usually quieter than social media makes it seem. It is not always visible through luxury purchases or expensive lifestyles. Sometimes, it looks like having savings prepared for emergencies. Sometimes, it means sleeping peacefully without worrying about unpaid debt. Sometimes, it is simply the freedom to enjoy life without feeling financially afraid every single month.

People who eventually improve their finances are not always the highest earners in the room. Often, they are simply the ones who became more honest about their habits, more patient with their progress, and more intentional with the choices they repeated every day.