MySSS Card Application 2026: The Complete Step-by-Step Guide

Getting your MySSS Card in 2026 doesn't mean a half-day trip to a crowded SSS branch anymore. The whole process now runs through your phone or laptop, using facial verification, your National ID, and a partner bank app — and if you don't know the order of operations ahead of time, it's easy to get stuck on a single error screen.

This guide walks through the full MySSS Card Application 2026 process: who qualifies, what the card actually does once it arrives, what it costs (usually nothing), and what to do when the system rejects your photo or flags a data mismatch.

It's written for three kinds of readers: members who still carry an old plastic UMID card and aren't sure if they need to upgrade, first-time SSS members who've never had a physical ID from the agency, and anyone whose application stalled halfway through the bank's e-KYC step.

By the end, you'll know which documents to have on hand, how long the card realistically takes to arrive, and which SSS branches are actually worth a visit if your account needs a manual fix.

For over a decade, the Unified Multi-Purpose ID was the standard government ID for SSS members. That's changed. As part of the country's broader move toward digital governance through the PhilSys national ID system, SSS has stopped producing standalone UMID cards at the branch level. Walk into a branch today asking for a fresh UMID biometric capture, and you'll be told to apply online instead.

Its replacement is the MySSS Card, built in partnership with commercial and rural banks like RCBC (through DiskarTech), UnionBank, and EastWest Rural Bank. Where the old UMID was just a photo ID with a chip, the MySSS Card does double duty: it's your official SSS-recognized ID and an EMV-chip Visa or Mastercard debit card at the same time.

Once you activate it, the card becomes your default disbursement account inside the SSS system. Salary loans, maternity benefits, sickness allowances, and pensions all land directly in the linked bank account. You no longer have to log in separately to the old Disbursement Account Enrollment Module just to register where your money goes.

Say you're a member who filed a maternity claim back in 2023 through the manual DAEM process — that enrollment still works, but it's no longer the path SSS is steering people toward. If you apply for the MySSS Card later, the new account it creates will override whatever bank details you had on file before, so it's worth knowing that going in rather than being surprised when your next benefit lands somewhere new.

Because the 2026 process is fully digital, SSS no longer captures biometrics manually at branches for this card. Instead, the system checks your member profile against the Philippine National ID registry. That means the prerequisites aren't really about paperwork you bring with you — they're about whether your existing records already line up.

First, your SSS number can't be tagged "Temporary." If you registered online years ago without ever presenting a physical PSA Birth Certificate at a branch, your account is likely still temporary, and the card application simply won't be available to you until that's fixed in person. Second, you need active credentials on the My.SSS web portal, since the entire application happens there.

Third, you'll need a PhilSys National ID — and it doesn't have to be the physical card. A digital ePhilID is accepted too, which matters if your printed PhilID is still stuck in the delivery backlog many applicants experienced in prior years. Fourth, and this trips up more people than anything else: your full legal name, middle name, suffix, and birth date have to match letter-for-letter between your SSS profile and your National ID.

A common scenario looks like this: a member's SSS record lists "Dela Cruz" as one word while the National ID has it as two words, "De La Cruz." That tiny difference is enough to fail the automated check. It's not a sign anything is wrong with your identity — it's just a database mismatch, and it's fixable, which we'll cover in the troubleshooting section further down.

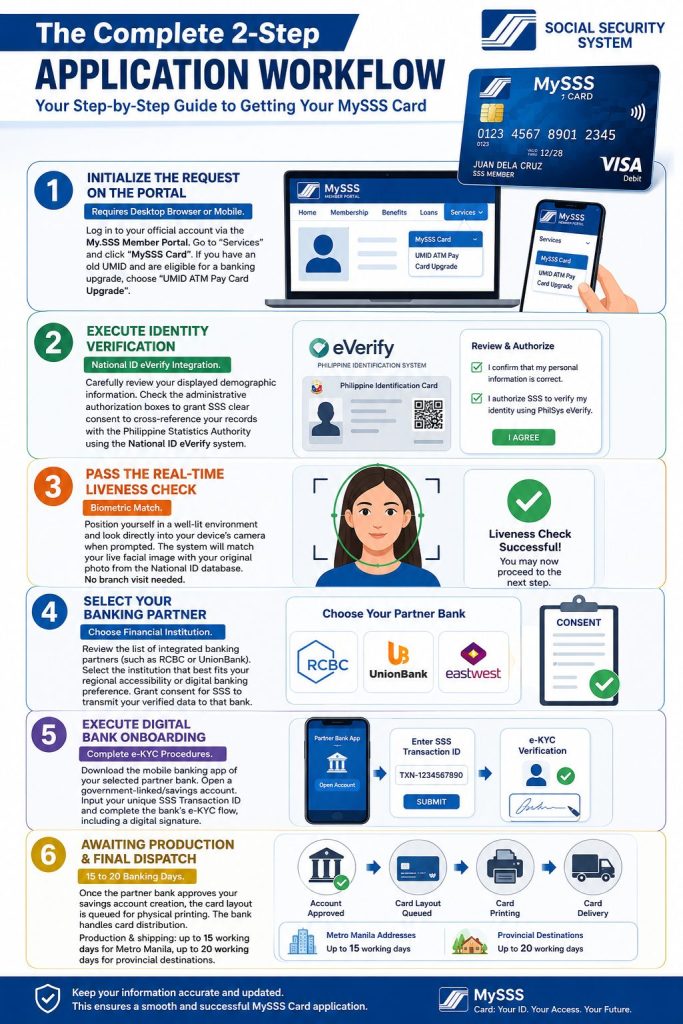

The process splits into two phases: identity verification inside the SSS portal, then onboarding with your chosen bank. Start by logging into the My.SSS Member Portal, hovering over "Services," and clicking "MySSS Card." Legacy UMID holders who qualify for a direct upgrade will see a separate banner instead, labeled "UMID ATM Pay Card Upgrade" — click that one if it appears.

Next comes identity verification. The portal displays your demographic details and asks you to authorize SSS to cross-check them against the Philippine Statistics Authority using the National ID eVerify system. After that, you'll go through a real-time liveness check: sit in good lighting, look at your camera, and let the system match your live face against your original National ID photo. There's no branch photo capture involved at all.

Once verification clears, you'll pick a partner bank — RCBC, UnionBank, or EastWest, depending on what's offered in your case — and authorize SSS to send your verified details to that bank. From there, you download the bank's app (DiskarTech for RCBC, or UnionBank Online, for example), open a government-linked savings account, enter the SSS transaction ID you were given, and complete the bank's own e-KYC steps, including a digital signature.

Picture a member who finishes the SSS side on a Monday morning and downloads the bank app that same afternoon. If the e-KYC submission goes through cleanly, the bank approves the account, queues the card for printing, and handles shipping from there — SSS itself isn't involved in delivery at all, which matters later if your card is running late.

Here's the part most members are relieved to hear: for the large majority of applicants, the MySSS Card costs nothing. SSS absorbs the administrative printing cost for first-time applicants, and the same applies to legacy UMID holders who complete the upgrade through the online automated invite rather than a third-party route.

The one scenario where you'll actually pay something is replacement — if your card is lost, damaged, or stolen, expect a fee in the ₱200 to ₱250 range, with the exact amount varying slightly depending on your partner bank's own card-issuance rules. That's still considerably less than what most commercial banks charge for a standalone debit card replacement.

On the banking side, partner banks waive the standard maintaining balance requirement for SSS-linked accounts, so you won't be penalized for keeping the balance at ₱0 between benefit credits. That's a meaningful difference from a typical savings account, where falling below the minimum balance usually triggers a monthly fee.

Think of a member who applies the moment they're eligible, never loses the card, and never needs a replacement — for that person, the entire journey from application to a working bank-linked ID costs exactly ₱0. The fee only shows up if something goes wrong physically with the card itself, not from the application process.

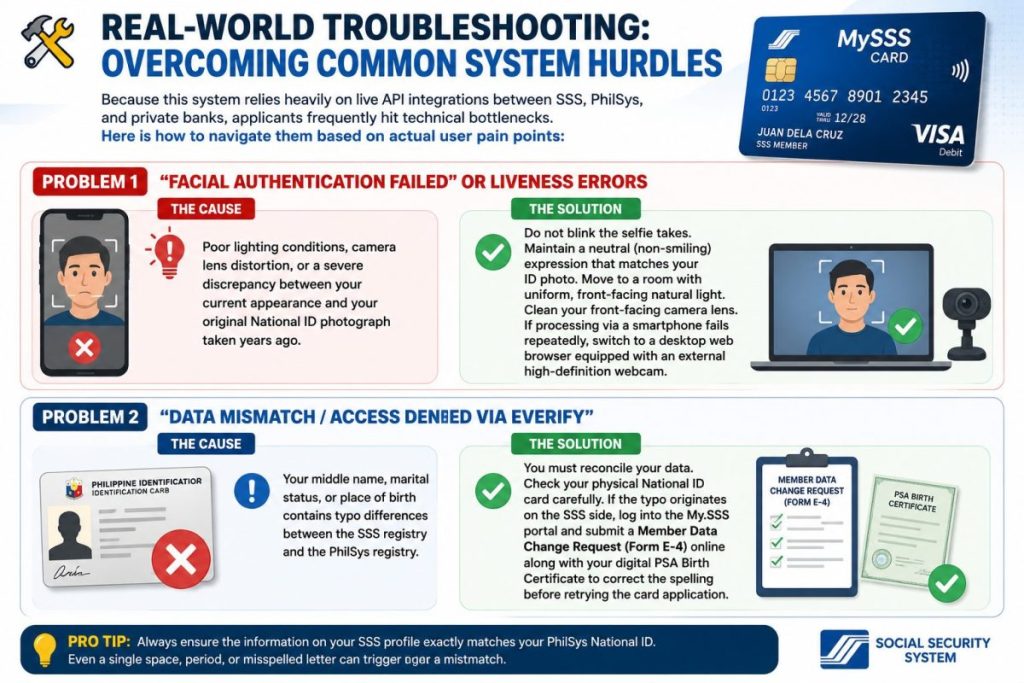

Since this system leans on live integrations between SSS, PhilSys, and private banks, hitting a snag somewhere in the chain isn't unusual. Most issues fall into one of two buckets: the facial liveness check fails, or the eVerify data match fails. Neither one means your application is permanently stuck — both have a clear fix.

Facial authentication failures usually come down to lighting and camera quality rather than anything wrong with your identity. Backlighting from a window behind you darkens your face and confuses the match. A dusty or smudged front camera lens does the same thing. If your phone keeps failing the check after a few tries, switch to a desktop browser with a decent external webcam — it often clears on the first attempt.

Data mismatch errors through eVerify happen when your middle name, marital status, or place of birth doesn't match exactly between the SSS registry and PhilSys. If the discrepancy traces back to the SSS side, you'll need to log into My.SSS and file a Member Data Change Request, known as Form E-4, along with a digital copy of your PSA Birth Certificate, before trying the card application again.

Take a member who's tried the liveness check four times in a dim bedroom with a window glaring behind them — switching to a well-lit kitchen table in the early afternoon and wiping the camera lens clears it on the next attempt almost every time. It sounds too simple to matter, but lighting genuinely is the most common fix.

Most applicants never need to set foot in an SSS office for this. But if your account is locked as Temporary, or if your data correction is too complex for the online Form E-4 process, a branch visit becomes necessary. Since you're already making the trip, it's worth picking a branch near somewhere worth going afterward instead of treating the whole day as wasted time.

The SSS Diliman Central Office on East Avenue in Quezon City is the headquarters branch, and it's generally the most reliable spot for clearing complicated record-history issues. Once you're done, the Quezon Memorial Circle is a short ride away, and the quiet residential streets of Maginhawa are nearby if you'd rather walk somewhere green.

If you're in Makati, the corporate branch sits right inside the Ayala Avenue financial district, which makes it easy to slot into a workday. The Ayala Triangle Gardens are right there for a quick walk afterward, and on a Saturday morning the Salcedo Weekend Market is worth the short stroll too.

Members in Northern Mindanao have it especially convenient — the SSS Cagayan de Oro branch sits inside Centrio Mall, so you can step straight from your appointment into air-conditioned shops, or head to the historic Vicente de Lara Park to sit under its old mahogany trees.

A few small decisions can shave days off your application and keep your only real cost at ₱0. Here's what experienced applicants do differently.

Check your SSS membership status first, confirm your name matches your PhilID letter-for-letter, and you'll have everything you need to complete the MySSS Card application in a single session. For most members, it costs nothing and takes less than an hour — and the card that arrives gives you a working government ID and a bank account in one.